Long-term, part-time employees may now be eligible to participate in your 401(k). Is your plan ready?

Making part-time employees eligible for retirement benefits was a positive step brought about by the SECURE Act. Now, it’s time to ensure your plan is following the right steps for this opportunity.

The Setting Every Community Up for Retirement Enhancement (SECURE) Act (known as SECURE 1.0, later updated by SECURE 2.0) extended eligibility for 401(k) plans to certain long-term part-time (LTPT) employees. Now is the time to ensure your plan is recognizing eligible service and providing LTPT employees with this benefit.

We understand that the provisions of the SECURE Act legislation can be complex. Here, we answer some questions and break them down so you can ensure your plan is accurately administering your 401(k) plan for eligible part-time employees. Information specific to Puerto Rico Only plans is available here.

What are the primary changes?

In 2024, LTPT employees must have three consecutive years of eligible service to participate in the 401(k) plan. In 2025, this requirement will be reduced to two years. These changes do not affect other requirements, such as whether the employer wants to offer employer contributions and/or include these employees in certain nondiscrimination tests.

For the plan year 2024

For the 2024 plan year, 401(k) plans in effect before 2021 will be subject to a three-consecutive-year eligibility service requirement. Service prior to 2021 is disregarded for vesting purposes so that the eligibility and vesting service requirements are harmonized.

For the plan year 2025

Beginning with the 2025 plan year, the three consecutive-year eligibility service requirement will be reduced to two consecutive years. Service prior to 2021 is disregarded for vesting purposes.

ERISA 401(k) Puerto Rico Only plans

SECURE Act 2.0 expanded the new provision for part-time employees to include ERISA 401(k) Puerto Rico Only plans beginning with plan year 2025. A two consecutive-year eligibility service requirement applies. Service prior to plan year 2023 is disregarded.

Who is eligible?

An LTPT employee becomes eligible for 401(k) provisions when they complete at least 500 hours of service every 12-month eligibility service computation period over three consecutive years, which, as stated above, reduces to two consecutive years for the 2025 plan year.

The eligibility service window applies for plan years beginning after December 31, 2020, and excludes service before that.

Employers maintaining a 401(k) plan may need a dual eligibility requirement under which an employee must complete either a one-year of service requirement (1,000 hours of service during the 12-month eligibility service computation period) or the required consecutive years of service in which the employee completes at least 500 hours of service in a 12-month eligibility service computation period.

What are they eligible for?

The new LTPT provision allows your eligible employees to make deferral contributions to your 401(k) plan. As a plan sponsor, however, you may still require the employee to satisfy the minimum age requirement, and you can also decide whether they will receive any employer contributions.

Are there exceptions?

Yes, there are a number of exceptions:

- Plan type: It includes 401(k) plans for plan years beginning in 2024 and ERISA 401(k) plans for plan years beginning in 2025 but excludes employees covered by a collective bargaining agreement.

- Plan design: Some plan designs will not be affected by the LTPT employee provision. For example, if a plan allows immediate eligibility or requires a short service requirement, such as three months or less, then the LTPT employee provision will not apply since employees will be eligible before completing 500 hours of service.

- Plans not tracking employee hours: Some 401(k) plans track employee hours to determine eligibility, but others use the “elapsed time method.” For example, if a plan has a one-year elapsed time eligibility service requirement, the employee won’t need to work a certain number of hours but must still be employed on their one-year employment anniversary date to satisfy the plan’s eligibility service requirement. The LTPT employee provision will not apply to those employees since they will be eligible to participate in the plan after they satisfy the plan’s age, service, and entry date requirements.

How does eligibility get calculated?

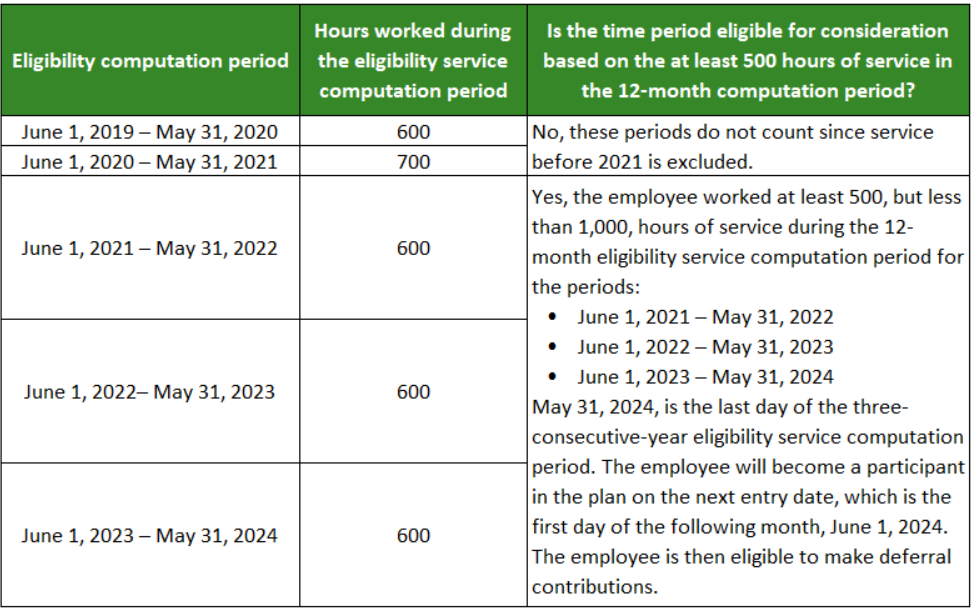

Eligibility is tracked using a 12-month “service computation period.” Here are two different scenarios for calculating service for a 25-year-old employee.

Example One:

A plan sponsor has a 401(k) plan with a December 31st year-end. It counts hours of service from the date of hire through the employee’s anniversary date. The plan has a requirement for one year and 1,000 hours of service, with monthly entry dates on the first of each month. This 25-year-old employee’s date of hire is June 1, 2019, and their hours of service for the past few years are listed in the table below.

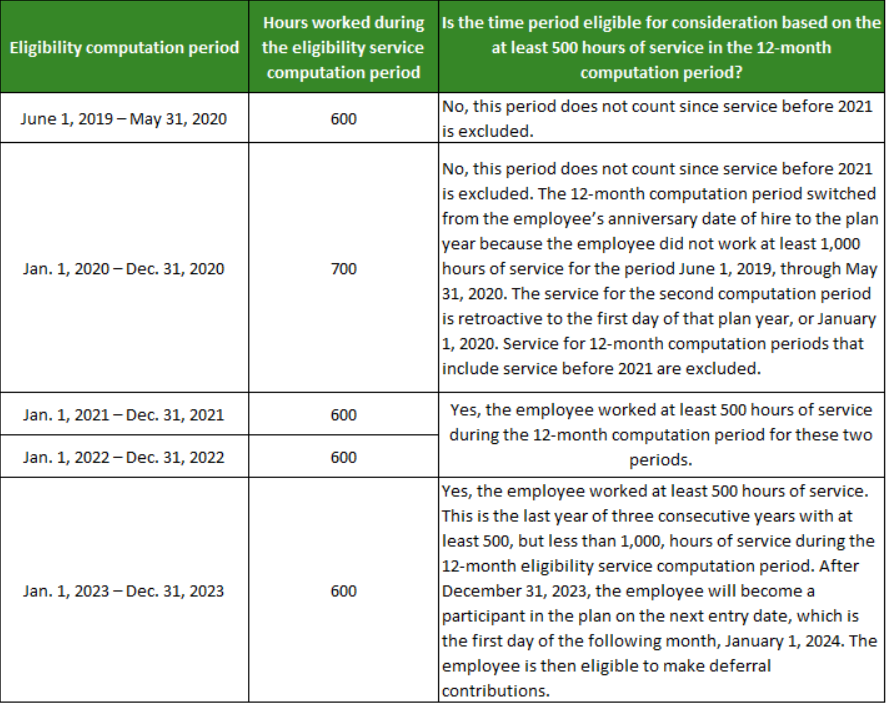

Example Two

Now let’s look at the same employee, except that the eligibility computation period switches to the plan year, from January 1st through December 31st, if they don't complete 1,000 hours of service during the first 12-month eligibility service computation period from their date of hire.

Information for Plan Sponsors

Eligibility Tracking

Fidelity’s Eligibility Tracking service is updated to include LTPT employees who complete at least 500 hours of service in each 12-month eligibility service computation period over two consecutive years.

Plan sponsors determining eligibility for their LTPT employees should review their procedures and/or consult with their payroll provider to identify the impact of the new provision. Payroll providers currently sending Fidelity eligibility information for full-time employees should continue this practice. Additionally, new LTPT employee information may be required to be sent to Fidelity. The applicable data required to be submitted to Fidelity is identified in the table below.

Note: Employee eligibility data will be required when an employee satisfies the service requirement for:

- 500 service hours in 2 consecutive years, AND if the employee later satisfies

- 1,000 service hours in 1 consecutive year

Employer Contributions

The LTPT employee provision allows plan sponsors to include or exclude LTPT employees from receiving employer contributions. Fidelity’s best practice is to exclude LTPT employees from receiving any employer contributions unless directed otherwise.

Plan sponsors using Fidelity’s Employer Contribution Calculation service will need to provide us with direction to make changes to their current employer contribution calculation for their LTPT employees if you choose to include LTPT participants. Please contact your Fidelity representative to discuss this further and determine if any changes will be required.

Plan sponsors calculating their own employer contributions should review their procedures to determine the impact of the LTPT employee provision on their calculation and discuss this with their payroll provider.

NetBenefits® has been updated to reflect generic participant information based on plan design.

Vesting

Fidelity Vesting service (actual hours of service) is being updated to review an employee’s service history once they satisfy the LTPT eligibility provision. All years of service in which the employee completes at least 500 hours of service in a vesting computation period will be counted, excluding appropriate service years. The plan may also be required to send a new LTPT Employee Attained Years value, when applicable. The data requirements are identified in the table below. Additional data elements may be required for other vesting methods.

New LTPT Employee Data Requirements

Eligibility and Vesting Data Elements

Four new data elements have been added to support the LTPT employee provision to identify employee’s eligibility, entry, and vesting dates.

In addition, Eligibility Date must be provided to Fidelity when an employee satisfies the LTPT rule, then later satisfies the standard eligibility rule (1,000 service hours in 1 year).

Sending Data to Fidelity

The following traditional channels will continue to support the new LTPT employee data elements:

- Electronic Data Transmission

- Plan Sponsor Webstation — File Upload

- Plan Sponsor Webstation — Participant Overview - Employment Information tab

Employee Communication and Enrollment Material

LTPT employees will continue to receive timely enrollment and plan communication material. Please contact your Fidelity representative to discuss communication materials when choosing to include LTPT employees in employer contributions.

Testing Services

Under the LTPT employee provision, plan sponsors can elect to include or exclude LTPT employees from nondiscrimination testing. Fidelity’s best practice is to exclude LTPT employees unless directed by plan sponsor.

Our Testing Group will use the LTPT employee data stored on Fidelity’s recordkeeping system for plans using Fidelity’s Eligibility Tracking service. Plan sponsors determining their own LTPT employee eligibility must provide the employee eligibility data to Fidelity in a timely manner when testing is performed by Fidelity.

Plan Sponsor Webstation Reporting

The new LTPT employee data elements were added to Plan Sponsor Webstation under the Create Reports section. You may create the relevant reports at your discretion. A Fidelity standard report identifying LTPT employees is also available.

Additional considerations

Your organization should already be compliant with SECURE 1.0.

Please review your internal procedures to ensure you are accurately tracking service hours for the appropriate computation periods. We also recommend that you consult with your legal counsel and/or benefits consultant to prepare for the changes and consider the impact of any future legislative change or IRS guidance.

Fidelity will, of course, keep you posted on any new developments. In the meantime, if you have any questions, please contact your Fidelity service team.